When Marc Rowan and David Haber Missed the Elephant

Apollo's CEO and a16z's GP correctly identify the gap between venture capital and private equity. Their solutions address yesterday's problems.

Marc Rowan did not set out to identify a structural flaw in private capital. He was talking about retirement income. David Haber was referencing a twelve-year-old essay.

Somewhere in between, they stumbled into the right problem. Both could see that something new is emerging. Neither could name it.

Haber’s observation was clean. The businesses AI is producing now - defense, energy, robotics, manufacturing: are capital-intensive in ways software never was. They will outgrow venture equity. They will need Apollo. His question to Rowan was direct: what do these companies need to do to become investable by you?

Rowan’s answer began with a confession. Apollo is not capital-constrained. It is idea-constrained. “We can only invest as fast as we originate, as fast as we create.” A trillion dollars in AUM. The binding limit is not money. It is worthy investments. Auctions don’t solve this — you arrive late, pay market price, remain a participant. “I want to be a principal,” he said. “I want to own the upside for as much of the asset as the market will allow.”

And then, almost in passing: “I think really good entrepreneurs are going to end up in partnership with entrepreneurs of another type — those who are financial entrepreneurs.”

He could see the shape. He could not see the form.

What followed was instructive. Pressed for solutions, both men reached for the tools they already hold. It was not enough.

Apollo opens a second headquarters near the growth ecosystem. Earlier engagement with founders. Better alignment between venture and credit. a16z helps portfolio companies think about capital structure sooner. Tighter pipelines. Smarter screening.

Real moves. None of them the answer.

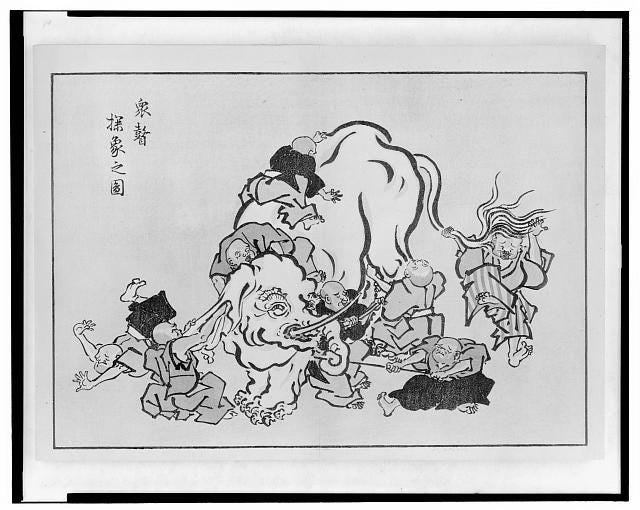

This is the blind men and the elephant. Rowan touches the trunk and describes a rope. Haber touches the leg and describes a tree. Both descriptions are accurate. Neither describes the animal.

Apollo is a financing and acquiring machine. It cannot build. It has no mechanism for originating ventures from inception: for installing the governance, the demand architecture, the exit design that makes a venture PE-investable before it becomes a company.

a16z is a funding and advising machine. It cannot transform risk profiles. A Series B defense-tech company does not become an Apollo asset because a16z introduced the founder to Rowan. The asset class is wrong. The governance is wrong. The exit architecture was never defined.

Both firms can see the destination. What’s missing is the way to get there.

This is not a criticism. It is a description of how worldviews work. You solve problems with the tools you have. When the problem requires a tool you don’t possess - one that doesn’t fit your existing architecture - you make the existing tools work harder. You call it progress.

Rowan and Haber are not slow. They are, in the precise sense, bound by what they can see from where they stand.

What they missed is not a feature. It is not a process improvement or a tighter feedback loop between Sand Hill Road and Midtown Manhattan. What they missed is a model.

The answer to Haber’s question — what do these companies need to do to become Apollo-investable — is not found in better staging or earlier introductions. It is found in rethinking what a venture is, and how it is built. Disruptive innovation, treated as a strategically designed and grown asset from inception rather than a bet that matures into legibility, changes the logic entirely. Demand confirmed before capital is committed. Exit architecture defined at structuring. Failure conditions priced in from day one. The result is not a better venture. It is a different asset class: one that carries venture-scale return potential at a risk profile PE can actually underwrite. That is not an incremental improvement on existing models. It redraws the playfield. It defines the next wave of long-term, strategic innovation, not as an accident of survival, but as a designed outcome.

Rowan described the problem it solves. Haber described the market that needs it. Neither could see it from where they stand.

The most interesting thing about their conversation is not what they said. It is what they almost said.

They were one step away. The gap between Apollo and a16z has a name. The partnership between financial entrepreneurs and venture entrepreneurs has an institutional form. The asset class they are both circling has a methodology behind it.

They stumbled into the question. Someone else will have to answer it.

A New Science of Venture Building is a demand-first venture building methodology designed for exactly the gap described in this piece.